Record-high input costs.

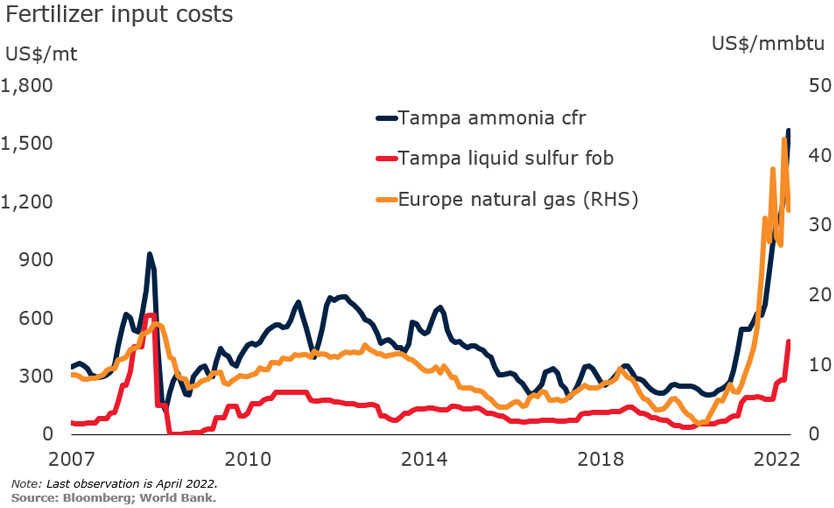

Rising natural gas prices, especially in Europe, led to widespread production cutbacks in ammonia—an important input for nitrogen-based fertilizers. Similarly, soaring prices of coal in China, the main feedstock for ammonia production there, forced fertilizer factories to cut production, which contributed to the increase in urea prices. Higher prices of ammonia and sulfur have also driven up phosphate fertilizer prices.

Sanctions and export restrictions.

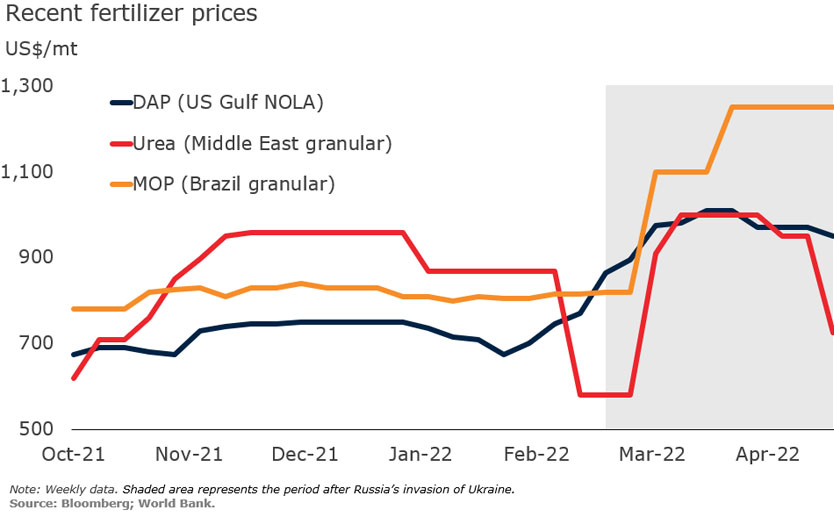

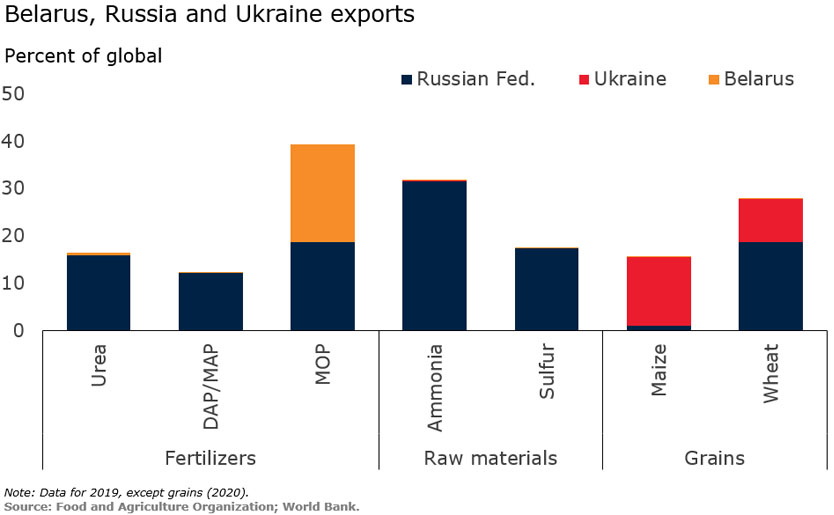

Fertilizer prices rose in response to the war in Ukraine, reflecting the impact of economic sanctions and disruptions in Black Sea trading routes. Russia accounts for about 16% of global urea exports and 12% of DAP and MAP exports, while Russia and Belarus together make up two-fifths of global MOP exports. Adding to supply concerns, China has suspended exports of fertilizers until at least June 2022 to ensure domestic availability.

Supply disruptions.

Although urea and DAP prices have retracted in recent weeks due to lower tender offers in India as buyers await clarity on Indian fertilizer subsidies, potash prices show no signs of easing. Potash supply shortages and uncertainty have increased following fresh sanctions on Belarus and Russia (on top of the sanctions imposed on Belarus last year). Moreover, Lithuania has halted the use of its railways’ network to transport Belarusian potash to the port of Klaipeda, which typically handles 90% of Belarusian fertilizer exports.

Robust demand.

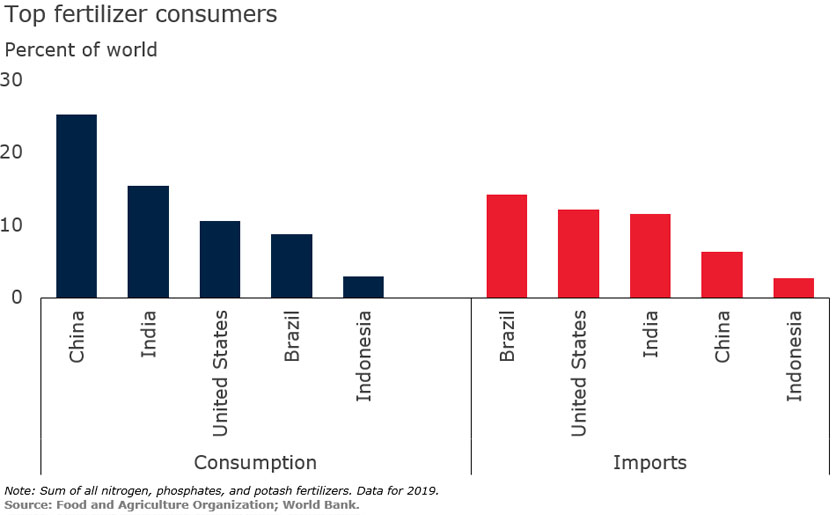

Global fertilizer consumption has remained strong throughout the COVID-19 pandemic. Brazil and the United States have allocated record acreage to soybean (a fertilizer-intensive crop). Demand is also strong in China due to increased feed use, especially maize and soybean meal, as the country is rebuilding its hog herd population following the African swine fever outbreak. Fertilizers are now at their least affordable levels since the 2008 global food crisis, despite higher crop prices, which may limit fertilizer use.

Outlook and risks.

Urea prices are expected to remain at historically high levels for as long as natural gas and coal prices remain elevated. Similarly, DAP prices are projected to remain high until ammonia and sulfur prices ease. Apart from input costs, risks to the outlook depend on whether China’s urea and DAP exports will resume after June. For potash, prices are anticipated to remain historically high through the next year unless supply returns to international markets from Russia and Belarus.

Source: blogs.worldbank.org